A common MSP business model is becoming clearer: providers are moving beyond break-fix or pure infrastructure support into recurring managed services, broader technology stacks, cybersecurity, cloud, compliance and ongoing customer enablement. That shift matters because the market is no longer niche or uniform. Our research forecasts the European MSP market at roughly EUR120bn in 2025, rising to around EUR220bn by 2030. That figure should be read as managed-services market value, not total channel throughput: low-margin hardware resale and other pass-through product revenues may sit inside an MSP’s commercial activity, but they should not be used to inflate the underlying size of the managed-services market. Just as importantly, large MSPs alone already account for about 65% of market spend, and medium plus large providers together represent the clear majority. However, before the industry can talk clearly about the European MSP market, it must answer a simpler question: what size is the MSP?

That question matters because the MSP market is now being measured by a growing set of stakeholders: service providers, vendors, suppliers, distributors, investors, buyers, and event organizers. Many already have their own way of calculating the size of the opportunity. Some look at revenue, others at headcount, customer base, recurring revenue, vendor relationships, geography or acquisition potential. But without a simple shared framework, the market becomes harder to compare, harder to benchmark and harder to serve.

This is especially important as M&A becomes a stronger force in the MSP market. Consolidation is reshaping the sector, but consolidation only becomes easier to understand when the industry has a common view of the market’s basic demographics: how many MSPs exist, how large they are, where they sit geographically and how their needs change as they scale. A clear size-tier framework does not replace more detailed analysis, but it gives the ecosystem a practical starting point.

For MSPs themselves, the value is also direct. Size tiers help providers compare where they stand against the wider market: whether they are still founder-led and local, moving into a more structured growth phase, building management layers, or becoming a larger cross-border platform. For MSP GLOBAL, the same framework helps us group content, networking and vendor conversations more intelligently, so providers get more relevant insight for their stage of growth.

Four growth stages, one diverse market

MSPs of different sizes are addressing a market whose customers don’t have uniform needs. A founder-led five-person business trying to professionalize its offer is operating under very different conditions from a 70-person firm building management layers, expanding into new geographies, and weighing acquisition opportunities. A local MSP and a cross-border consolidator may both sit under the same umbrella term, but they do not learn, hire, buy, compete, or grow in the same way.

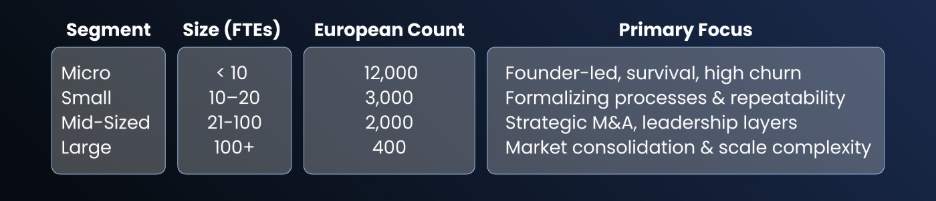

That is why MSP GLOBAL uses four clear size segments, from micro MSPs with fewer than 10 FTEs, to small MSPs with between 10 and 20 FTEs, then mid-sized MSPs with 21 to 100 FTEs, and finally large MSPs with more than 100 FTEs.

These categories matter because the pressure points, growth patterns, investment priorities, and information needs of an MSP change materially as it scales. While no segmentation captures every business perfectly, this framework offers a clearer shared language for understanding a European market that continues to grow, consolidate, and change.

Our sizing points to a recognized universe of around 12,000 micro MSPs, 3,000 small MSPs, 2,000 mid-sized MSPs and roughly 400 large MSPs across Europe. The growth logic is different in each case. Micro MSPs are numerous but relatively flat as new entrants replace businesses that are acquired. Small MSPs grow steadily as they formalize. Mid-sized and large MSPs are shaped much more strongly by consolidation, M&A, and professionalization. At the same time, the mid-sized segment is becoming one of the main characters of the story: dynamic, acquisitive, increasingly sophisticated and central to where the market is going next.

Different sizes, different operating realities

MSPs of every size are facing a similar set of core pressures and challenges: keeping up with fast-changing technology, differentiating in a crowded market, building stronger business know-how, and responding to rising compliance and security demands. NIS2, DORA and wider cyber risk are only sharpening that pressure. But the way those issues are experienced is not uniform. For a micro MSP, the challenge may be doing everything at once. For a mid-sized provider, it may be deciding how to build specialist capability, manage leadership layers or use M&A as a growth lever. For a large MSP, it is often about handling complexity at scale without losing focus or momentum.

These differences also determine why MSPs come to MSP GLOBAL. Smaller providers are often seeking clarity, practical direction, vendor discovery and signals they can use immediately. Mid-sized MSPs are more likely to be looking for sharper benchmarks, better strategic context, and insight that informs decisions on structure, specialization, partnerships, vendor selection and growth. Larger providers tend to engage from yet a different vantage point: to pressure-test assumptions, read market direction, assess more complex partnership opportunities, refine vendor choices, deepen key relationships, and stay close to the conversations shaping the category.

That is what gives MSP GLOBAL its distinct value. At its best, it is not just a convening point, but a “home base” community for the European MSP industry: a trusted place for perspective, market intelligence, and thought leadership, with the authority to speak to providers at different stages of scale and maturity.

Why segmentation must extend beyond events

Seen this way, generic channel coverage can feel too blunt: “MSPs” are often treated as one category, even though local operators, repeatable small businesses, strategic mid-sized providers and consolidating platform players all behave very differently. This is where MSP GLOBAL can help the industry move toward clearer size, focus, and maturity definitions that support better decisions across the whole ecosystem, from MSP strategy and vendor targeting to investment, partnership, and M&A activity.

It is especially valuable in Europe because maturity still varies significantly by geography. The UK is widely seen as the most developed MSP market, with Benelux and the Nordics also relatively mature. Markets such as Germany, France, and Italy are developing quickly, but many providers there are still earlier in the managed-services journey and local terminology remains more mixed. A better framework helps the industry compare apples to apples across borders instead of flattening different markets into one story.

It also helps MSPs benchmark themselves more honestly. A provider with 15 people should not be measured against the operating model of a 150-person platform, and a 70-person MSP should not be treated as if it has the same needs as a founder-led micro business. Clearer tiers make it easier to ask better questions: What should our next stage of maturity look like? Which peers are most relevant? Which vendors fit our current scale? Which content, data, and relationships will help us grow from here?

The year-round information gap

Our research also shows that this is fundamentally a question of year-round information need. MSPs are looking for market, product and regulatory information daily or weekly, yet they currently piece it together from industry news sites, newsletters, LinkedIn, online communities, vendor blogs, podcasts, webinars, analyst reports, and trade shows. That creates a clear efficiency problem: too many sources, too much noise, and too much time spent filtering rather than learning.

That is why the strongest signal in the research is not just about attendance. I: it is about authority and utility. Around 80% of MSPs expressed interest in a centralized information platform, 65% in frequent peer knowledge-sharing sessions, and 75% in an MSP directory. In other words, the market is asking for something more than a once-a-year touchpoint. It wants a trusted layer of content, peer exchange, and data that reflects how MSPs actually run and grow their businesses.

This is the wider role MSP GLOBAL can play for the market: becoming a valuable year-round source of segmented market intelligence for the European MSP community. That means explaining what is changing, what matters by segment, how providers in different stages of growth can benchmark themselves more accurately, and how the wider ecosystem can better understand the market it is trying to serve.

The MSP landscape is shifting fast. Get ahead by joining the brightest and the best at MSP GLOBAL. Your first step? Sign up for the newsletter to get your free ticket code and save €€€s.